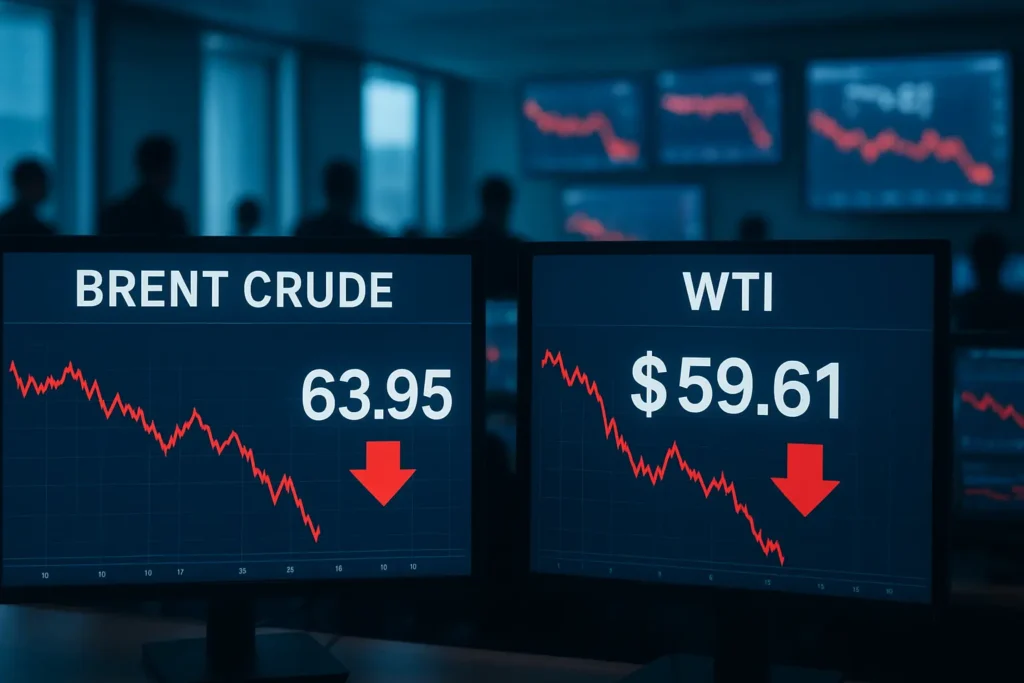

Oil prices fell on Monday, wiping out last week’s gains after loadings resumed at Novorossiysk, the key Russian export hub on the Black Sea. The reversal came following a two-day suspension triggered by a Ukrainian attack on the critical port. Brent crude futures dropped 44 cents to settle at $63.95 per barrel by 0751 GMT, while U.S. West Texas Intermediate (WTI) was trading around $59.61, down 48 cents or 0.8% from Friday’s close.

The price drop caught some traders off guard. Both benchmarks rose more than 2% on Friday, giving the week a modest gain after exports were suspended at the port and the neighbouring Caspian Pipeline Consortium terminal. That suspension was affecting roughly 2% of global supply, based on what industry sources and LSEG data showed. Markets got spooked, prices jumped, and then everything reversed course once operations restarted.

Novorossiysk port got back to work on Sunday. Two industry sources confirmed oil loadings picked up again at the Russian export hub, which moves huge volumes of Russia’s crude to buyers worldwide. The Black Sea location makes it strategically important—lose this port even temporarily and you’re talking about real pressure on global energy flows.

But here’s the catch. Ukraine’s stepped-up attacks on Russia’s energy infrastructure remain a serious concern for anyone watching supply chains. Ukraine’s military said on Saturday it hit Russia’s Ryazan refinery. Then Kyiv’s General Staff announced on Sunday it struck the Novokuibyshevsk refinery over in Russia’s Samara region. These aren’t isolated incidents anymore. Ukraine is systematically going after Russia’s energy capabilities with drone strikes, and that pattern suggests more disruptions are probably coming.

The refinery attacks matter because they limit Russia’s ability to process crude into products like gasoline and diesel. Even if the export terminals keep running, damaged refineries create bottlenecks that can ripple across markets.

So why did oil fall if there’s all this risk? Investors are trying to figure out the same thing. Part of it comes down to profit-taking. After Friday’s rally, plenty of traders wanted to lock in gains before the situation changed again.

Toshitaka Tazawa, an analyst at Fujitomi Securities, put it pretty simply. “Overall, the perception of oversupply from OPEC+ production increases remains,” he explained. Tazawa thinks WTI will probably stay near $60 a barrel, maybe fluctuating within a $5 range depending on news flow.

The market keeps monitoring how Western sanctions actually impact Russian supply and trade flows. Right now there’s this tension—geopolitical events should push prices up, but fundamental oversupply concerns keep pulling them back down. Speculators are being careful with their positions because nobody knows which force wins out.

What really moved things on Monday was simple logic. Once Novorossiysk reopened, the immediate threat to supply disappeared. Traders quickly shifted back to worrying about the bigger picture, which right now points toward too much oil sloshing around rather than too little.

The sanctions story got more complicated recently. The United States imposed new measures banning deals with major Russian oil companies Lukoil and Rosneft after November 21. The goal is pushing Moscow toward peace talks over Ukraine, though whether that works remains anybody’s guess.

Then President Donald Trump said on Sunday that Republicans are working on legislation to impose sanctions on any country doing business with Russia. He also said Iran may get added to that list, which would seriously complicate things. Secondary sanctions like these change the whole game because suddenly countries have to choose between buying Russian crude and maintaining access to U.S. financial systems.

For investors watching trade patterns, this creates massive uncertainty. Major buyers like India and China have been snapping up discounted Russian oil. If those flows get disrupted by sanctions, where does that oil go? And more importantly, where do those countries turn for replacement barrels?

Earlier this month, OPEC+ agreed to increase December output targets by 137,000 barrels per day—the same bump as October and November. They also agreed to hit pause on further increases in the first quarter of next year. The cartel is clearly trying to support prices without losing market share to U.S. shale producers who keep drilling regardless of what OPEC+ does.

ING released a report saying the oil market should remain in large surplus through 2026. That’s bearish for prices and explains some of the downward pressure. But ING also warned about rising supply risks—Ukraine’s attacks on Russia’s energy facilities being the obvious one.

The report mentioned something else concerning. Iran seized a tanker in the Gulf of Oman after it transited the Strait of Hormuz. That waterway handles about 20 million barrels per day of global oil flows. Any problems there send shockwaves through the entire market.

The latest positioning data tells an interesting story. Speculators increased their net long positions in ICE Brent by 12,636 lots over the last reporting week, bringing the total to 164,867 lots as of last Tuesday. According to ING, this was predominantly driven by short-covering—meaning traders who had bet on falling prices rushed to close those bets.

Why? Some participants seemed reluctant to stay short at the moment amid supply risks related to sanctions and geopolitical tensions. Even with oversupply concerns, betting on lower prices feels dangerous when Ukraine keeps hitting Russian energy targets and Trump threatens broader sanctions.

Meanwhile, back in the United States, the number of rigs drilling for oil rose by three to 417 in the week ending November 14. That data from oil services firm Baker Hughes came out on Friday and shows American producers aren’t backing off despite WTI sitting around $60. They’ve gotten good at making money at these price levels, which adds to the oversupply problem.

Looking ahead, a lot depends on how aggressive Ukraine gets with attacks on Russia’s energy infrastructure and whether the Trump administration really follows through on secondary sanctions. For now, markets seem to think supply worries take a back seat to oversupply fears. But that could flip quickly if another major export terminal goes offline or sanctions actually start biting harder.