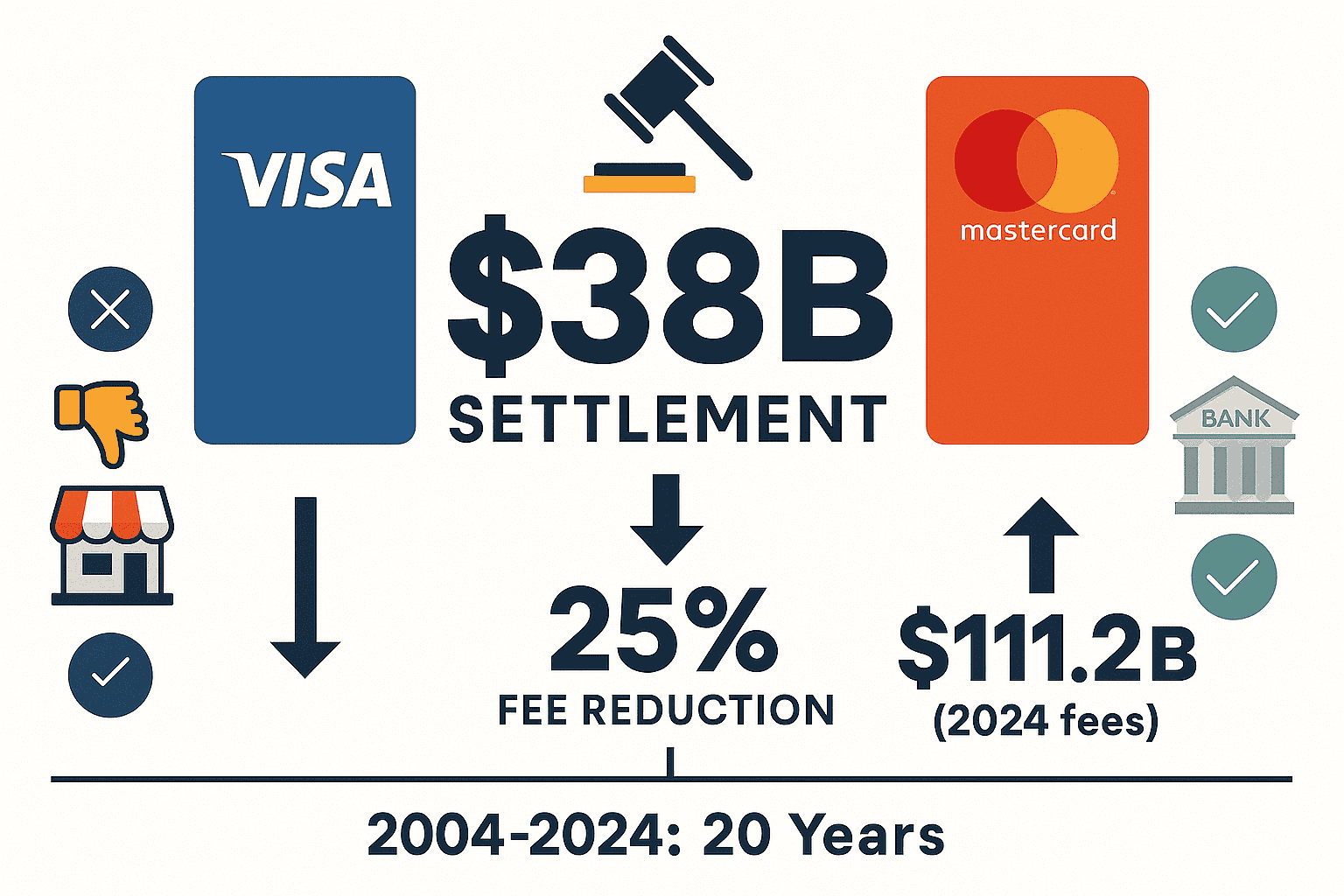

Visa and Mastercard announced a revised $38 billion settlement with merchants Monday, ending 20 years of litigation over swipe fees that businesses claim violate U.S. antitrust laws. U.S. District Judge Margo Brodie in Brooklyn, New York, had rejected a smaller accord worth $30 billion in June 2024 as inadequate, forcing the card networks to return with improved terms.

The revised deal aims to lower the fees merchants pay when customers use credit cards, but major merchant groups including the National Retail Federation and Merchants Payments Coalition maintain fierce opposition. They argue the agreement still allows Visa and Mastercard to charge too much, particularly for rewards cards that dominate the card market and represent 80% of card customers.

Judge Brodie delivered a stinging rejection of the earlier $30 billion settlement, calling the $6 billion in annual savings for merchants “paltry” relative to what the card networks could still extract from businesses. The judge faulted the accord for sticking merchants with the “Honor All Cards rule” requiring them to accept all Visa and Mastercard cards, or none.

The original deal would have reduced swipe fees, which are typically 2% to 2.5%, by only about 0.07 percentage points over five years. Fees remain above where they would be absent the antitrust violations, the judge concluded. Her concerns about the inadequate terms forced Visa, based in San Francisco, and Mastercard, headquartered in Purchase, New York, back to the negotiating table.

New Terms Offer Deeper Fee Reductions

The revised settlement calls for Visa and Mastercard to reduce swipe fees by 0.1 percentage point for five years, a modest improvement over the rejected proposal. More significantly, standard consumer rates would be capped for eight years at 1.25%, representing a more than 25% reduction from current levels that merchants face daily.

Two economics experts, including Nobel Prize-winning economist Joseph Stiglitz, estimate the changes can conservatively save merchants more than $200 billion over the course of settlement through 2031. The $38 billion settlement value reflects the projected reduction in fees businesses will pay when accepting credit cards. Merchants would also gain an “unfettered ability” to charge up to 3% in surcharges when customers pay by card, according to a court filing.

Card Categories Give Merchants New Control

Under the new terms, merchants can choose whether to accept U.S. cards in specific categories including commercial cards, premium consumer cards encompassing many rewards cards, and standard consumer cards. This provision addresses Judge Brodie’s criticism about the Honor All Cards rule that previously forced businesses to accept every card type.

The flexibility represents meaningful relief for merchants of all sizes, particularly smaller merchants who struggle with the collection of interchange fees. Visa said the deal provides more options for businesses to control how customers pay them, while Mastercard emphasized lower costs and simpler rules as key benefits. Neither company admitted wrongdoing in agreeing to settle, and their shares were little changed in afternoon trading.

Swipe Fees Have Quadrupled Since 2009

Interchange fees totaled $111.2 billion in the United States in 2024, up from $100.8 billion in 2023, according to the NRF. The fees have quadrupled from their level in 2009, creating mounting pressure on businesses that must absorb these costs or pass them to consumers.

“You can’t just suddenly tell more than 80% of your card customers you’re not going to take their cards,” said Stephanie Martz, the NRF’s general counsel, in an interview. “You would lose business.” The largest U.S. retail trade group contends merchants still pay too much, especially as rewards cards dominate the market and command higher swipe fees.

Banking Industry Supports Deal

The Electronic Payments Coalition, whose members include the card networks and large issuers such as Bank of America, Capital One, JPMorgan Chase & Co, and Citi Bank, supports the settlement. Executive Chairman Richard Hunt argues the deal would reduce swipe fees below those contemplated in a Senate bill sponsored by Democrat Richard Durbin of Illinois and Republican Roger Marshall of Kansas, which much of the banking industry opposes.

“You tell me the last time Walmart reduced any of its prices by more than 25%, and kept it for eight years,” Hunt said in an interview. However, Doug Kantor, general counsel of the National Association of Convenience Stores and executive committee member of the Merchants Payments Coalition, counters that the settlement prohibits merchants from negotiating prices set with different banks. The deal doesn’t give banks an incentive to lower rates they charge, but lets Visa and Mastercard “without any limitation” raise their own fees, he said.

What This Means for Your Business

The settlement still requires approval from U.S. District Judge Margo Brodie in Brooklyn, New York, who must determine whether the revised terms adequately address her concerns about the previous smaller deal. Businesses accused the card networks and banks of conspiring to violate U.S. antitrust laws through anti-steering rules that prevent them from directing customers toward cheaper means of payment.

Merchants ought to negotiate freely with card issuers, but the current structure limits their ability to secure competitive rates. The opposition from major merchant groups suggests the fight over swipe fees may continue even if Judge Brodie grants approval. The projected reduction through 2031 offers some financial relief, but whether it provides sufficient meaningful relief remains contested among merchants of all sizes who must navigate the complex world of card networks and interchange fees.