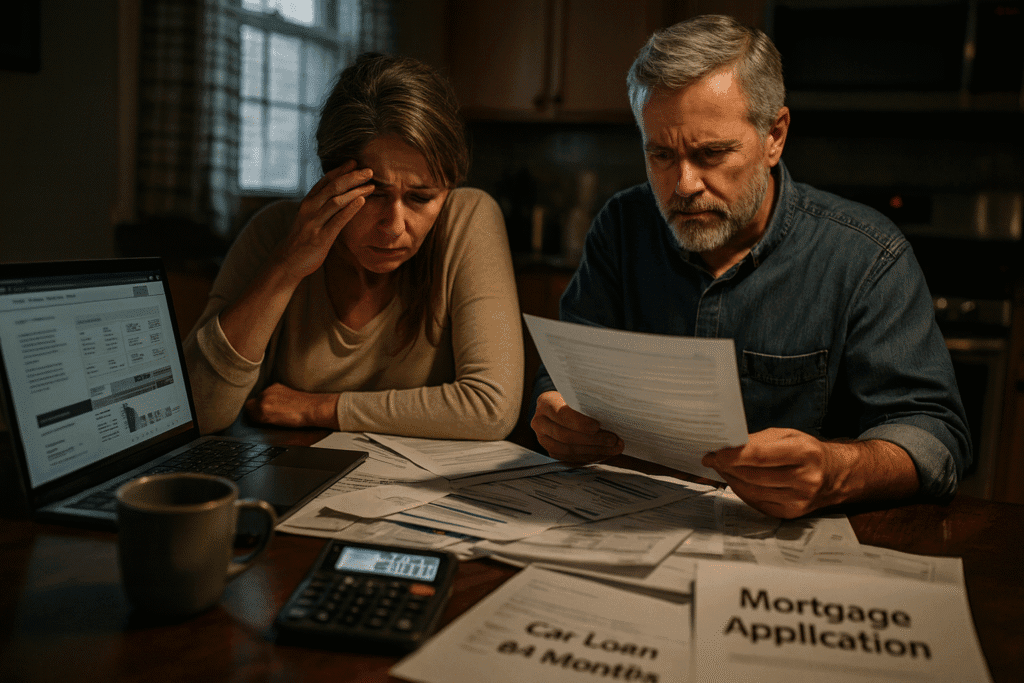

Stubborn inflation continues to make the cost of living unbearable for many Americans, forcing millions into longer-term debt just to afford basic purchases. From 50-year mortgages to seven-year car loans, inventive solutions have emerged with a common theme: putting consumers deeper in debt while delaying true ownership indefinitely. These financial products promise relief but deliver dependency instead.

Bill Pulte, director of the Federal Housing Finance Agency, remarked over the weekend on X that President Donald Trump sees the 50-year mortgage proposal as a “complete game changer” for struggling homebuyers. The latest example of this trend could lower monthly payments significantly, but the amount of interest a borrower would pay over 50 years would double what they’d pay at current rates on a 30-year loan—the traditional length of most mortgages. Assuming even the average American survives the entire life expectancy of around 80 years old, they’d have to get their mortgage by the time they’re 30 for a shot—albeit slim—at reaping the benefits of homeownership before they die.

“Generally speaking, you’re better off if you avoid longer-than-usual loan terms,” said Matt Schulz, chief consumer finance analyst at LendingTree. The number of inventive solutions may help ease financial anxiety in the immediate future, but they also do significant damage to consumer stability over the long haul. Financial experts warn that these extended terms create generational debt cycles that trap families for decades.

One potential game changer comes from the auto industry, where seven-year car loans have become an increasingly popular option as the average price of a new vehicle hits a record of more than $50,000. Cars tend to lose value rapidly when you drive them off the lot, so with a seven-year loan, you run the risk of owing more on it than it is worth—not a situation anyone wants. This explosion of extended financing options has normalized taking on longer-term debt for purchases that depreciate quickly, trapping buyers in a cycle where they’ll never achieve true ownership before needing a replacement vehicle.

The problem extends beyond just auto loans—all major forms of debt, including mortgages, auto loans, and student loans, have hit record highs according to the New York Fed, which has been tracking household debt since 2003. In total, Americans are shouldering $18.6 trillion in debt, up 3.6% from a year ago. This staggering figure represents a fundamental shift in how Americans finance their lives.

The explosion of buy now pay later (BNPL) options at online and brick-and-mortar retailers, including small purchases like food delivery offerings, has normalized delaying payment for everyday items. These services allow consumers to own goods by giving them an instant stream of funds to tap into, but younger ones especially are making purchases they otherwise may have been able to afford without credit. A Federal Reserve study published last year found that BNPL users reported lower overall financial well-being than those who don’t use these services.

The study revealed that adults who report using BNPL services “appear to be liquidity and credit constrained” and were “only likely to use” these options because they indicated they “used them because it was the only way to make” the purchase. Within the broader debt landscape, card debt has risen nearly 6% to $1.2 trillion, while the rate of borrowers who entered serious delinquency—meaning they’re at least 90 days behind on making payments—rose to 3% in the third quarter of last year, the highest level in a decade according to Fed data.

While renting has some advantages, there’s no upside equivalent to the wealth-building ownership provides when property values appreciate, generating equity that can be tapped later in life or used when people retire. Not to mention, there are tax benefits to owning a home, such as the ability to deduct mortgage interest payments from your tax burden—no such equivalent exists for rent payments. “Homeownership remains one of the most accessible ways for the average person to build wealth,” Schulz said. The wealth gap between homeowners and renters continues to widen each year, creating lasting economic inequality.

Yet prices remain so high that they’ve stayed elevated for several years, giving yet another segment of Americans pause about whether they’ll ever achieve this milestone. The pause many feel isn’t just about housing—it reflects a broader crisis where affordability has become so elusive that possible solutions only push true ownership further out of reach.

The week brought fresh evidence that these longer-term financing offerings can help address immediate affordability concerns while simultaneously ensuring you’ll spend decades paying for assets that may lose value or never truly belong to you. These inventive approaches share a troubling pattern: they transform one-time purchases into lifelong payment plans, fundamentally changing the relationship between consumers and ownership. The good news is that awareness of these traps gives you the choice to resist them and seek alternatives that build genuine wealth rather than perpetual debt obligations.